![]() 6 minute read

6 minute read

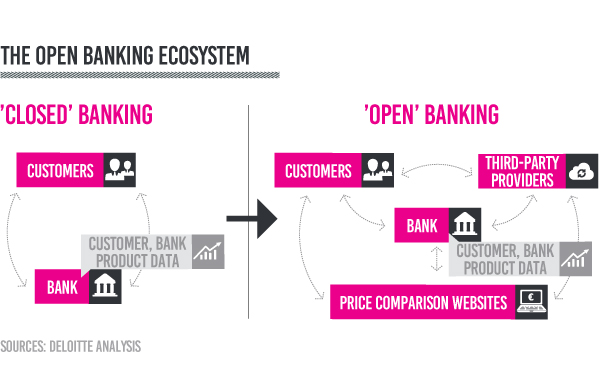

Due to a new regulation called PSD2, all banks in the EU must provide the financial data of their customers to a third party with the customer’s consent. This enables competing banks and FinTech companies to gain new customers if they can provide versatile enough services that ease the lives of their users. Through this new, secure way of transferring information between banks and third parties, payment methods become faster, and new innovative banking products will be introduced. Welcome to the world of open banking.

Reactions to regulations

The new regulations and open banking push the financial sector to change their game. Deloitte found that only 25% of European banks feel ready and confident about their strategic plans for the future. There are different ways major banks are embracing the disruption and solving related issues. Santander, for instance, is teaming up with small FinTech companies and start-ups. Goldman Sachs is protecting its assets by buying competitor companies. Bank of America has partnered with Microsoft to develop their tech abilities. However, rather than these changes being rapid, according to Deloitte research, the effects of PSD2 will be gradual and irreversible.

According to Fujitsu, 37% of European consumers say they would change their bank if it did not offer cutting-edge technology. Thus, to ensure a front row seat in the open banking ecosystem, banks need to become more innovative internally or collaborate with other companies, such as FinTechs. By developing its own innovative products, the bank keeps the ownership of the distribution and the interface. In 2017, 88% of incumbent banks were becoming worried of losing their revenue to third-party innovators. However, banks can ease the process of staying relevant by collaborating and sharing their customer access with third parties, instead of competing with them. This results in better customer experiences due to more diverse services. So far, according to Business Insider, 54% of incumbent banks have stated that partnerships with FinTechs have increased their revenue. These collaborations will also yield cost savings and refresh branding.

FinTech collaborations

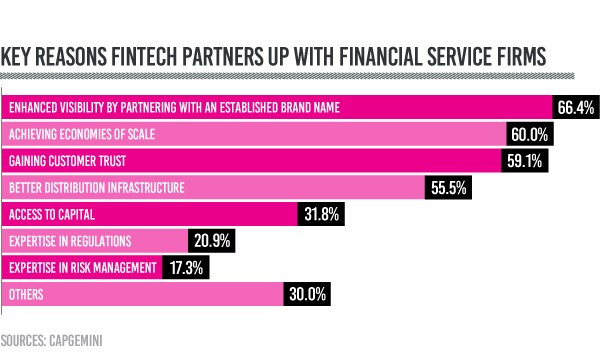

Where banks originally felt threatened, FinTech companies are enthusiastic about the opportunities open banking provides. According to a study by EY, 94% of FinTech companies see open banking as a major area of opportunity, and 81% of the respondents are already actively preparing for them. The World FinTech Report Survey of 2017 found that 66.4% of respondents see enhancing their visibility with an established brand name as the key reason for why FinTech companies want to partner with traditional financial services companies.

Finastra has developed a platform that helps 9,000 banks and FinTechs embrace the benefits of open banking together. The company launched Fusionfabric.cloud in 2017, which enables all creators of financial applications to collaborate within the three components of a global and digital marketplace. FusionCreator is a development environment for financial applications, that lets banks collaborate with FinTechs to build and access new capabilities. This has decreased the development time from months to weeks. FusionOperate, in turn, is a management system that allows users to operate applications in a secure cloud infrastructure. Finally, FusionStore is an online marketplace where banks can search, try and buy applications. Simon Paris, CEO at Finastra, said: “The move to a bank as a platform or banking as a service will redefine the future of financial services and we are at the forefront, bringing banks and Fintechs together to allow faster innovation at much lower costs. We are changing the way that financial services software is developed, deployed and consumed, like no one else – building the foundations of a completely new financial services ecosystem and marketplace, and thereby unlocking the potential of people and businesses alike.”

Digital shopping malls

New digital platforms and ecosystems will provide more extensive services to consumers. Additionally, companies outside the financial services industry will add their touch to these platforms. As the end result, these ecosystems will include multiple microservices that complement one another and provide a seamless journey through customers’ needs. In other words, they become virtual shopping malls where all the different services are within close reach. This makes taking care of everything related to finances faster and easier, and it can all be done remotely.

The Chinese digital platform, WeChat, is a great example of how easily users can manage their lives through a single app. It is used by 1 billion people, out of which 900 million are daily users. Within this ecosystem, consumers can manage their finances, communicate with business and private purposes, book transportation or doctor appointments, and even use virtual reality. The next step is to create a global platform similar to WeChat. Its establishment would enable the globalization of all these different services, while simultaneously giving companies a broader reach to new clients.

Platforms to educate individuals

When considering the benefits open banking has for individuals, a distinguished one is having strengthened possibilities for financial management. FinTechs and banks together have already developed apps that, for example, Yolt, that shows accounts from different banks in one place. Plum is an app that helps with budgeting, and TransferWise enables cheaper and faster international money transfers. There is even an app called Bankify that helps with a microbudget. Imagine how individuals could benefit from finding all these services within one application platform.

According to an OECD report from 2017, only 60% of adults in G20 countries reached the minimum target of financial literacy. The overall result is built from scores in financial knowledge and financial behaviors, as well as attitudes to long-term financial planning. Only 52% of respondents showed the minimum amount financially smart behaviors required. Banks, such as Univest, and other financial services have tackled financial illiteracy with education programmes in schools to ensure that the knowledge is learned early in life. Digital financial ecosystems could be an alternative to this process, as they can guide the user to spend and invest their money wisely.

However, consumers need to be careful when trusting these platforms because the information they get from third-party apps may not be impartial. Correspondingly, Helen Saxon, a chief monetary analyst at MoneySavingExpert.com warns: “They may find you an energy deal that saves you money, but there’s no guarantee they’ve searched the whole of the energy market to find the cheapest tariff. They may just offer deals from companies who pay them for new business.”